Key Takeaways:

- Diversifying income sources enhances financial resilience.

- Establishing reserve funds provides a safety net during economic downturns.

- Implementing strong financial controls ensures transparency and trust.

- Leveraging technology can streamline financial management and improve efficiency.

Introduction

Achieving lasting financial security is crucial for organizations and individuals alike. While the challenges may vary, sound financial management’s core principles apply to nonprofits and personal finances. For nonprofits, this means ensuring programs and operations can persevere through economic downturns or shifts in donor priorities. For individuals, it’s about maintaining stability amid job changes, unexpected expenses, or larger market shifts. Financial security, therefore, is more than just a good idea—it’s a foundation for resilience and opportunity. For comprehensive strategies endorsed by financial professionals, consider insights from Aaron Werner Raymond James.

In both cases, adopting a multifaceted approach is best. By focusing on revenue diversification, building reserves, strong financial governance, cutting-edge technology, and a proactive mindset, anyone can boost their economic resilience and prepare for a more secure future.

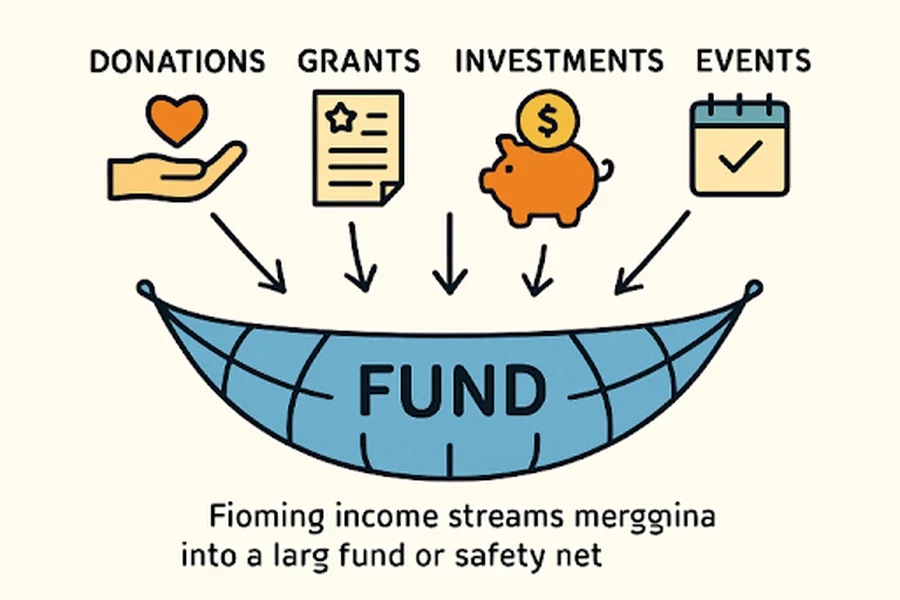

Diversify Revenue Streams

Depending on a single income source leaves both nonprofits and individuals vulnerable to sudden changes. Nonprofits often rely heavily on grants or a major donor—putting them at risk when funding priorities shift. Expanding to include individual contributions, corporate sponsorships, events, and fee-for-service models strengthens resilience. For individuals, side gigs, stock investments, and even rental income can create additional financial cushions that buffer against job loss or economic slumps. Broadening income sources means every setback has less impact, and new opportunities can be seized confidently.

Diversification is at the core of risk management strategies. According to Investopedia, spreading income streams minimizes risks related to any single revenue source while potentially increasing overall financial growth.

Build and Maintain Reserve Funds

The importance of a financial buffer cannot be overstated. For nonprofits, having accessible reserves equivalent to six months of essential expenses ensures continuation in crises or funding lapses. This means programs don’t have to slow down or stop when emergencies arise. Individuals, likewise, should target an emergency fund sufficient to cover three to six months of personal expenses. This provides peace of mind and prevents reliance on high-interest debt during financial shocks.

Cultivating strong reserve habits also helps organizations and people make proactive, rather than reactive, financial decisions. It allows for adapting to opportunities or riding out a difficult stretch without derailing long-term plans.

Implement Strong Financial Controls

Trust and transparency are non-negotiable in sustainable financial management. Nonprofits gain credibility and donor confidence when they adhere to robust practices, such as regular audits, financial reporting, and separating duties to avoid conflicts of interest or fraud. Likewise, individuals benefit from budgeting tools, setting clear financial goals, and regularly reviewing expenditures and savings. These habits shine a light on blind spots and prevent small issues from evolving into large ones.

Accountability Measures for Nonprofits

Periodic audits and transparent reporting are not only best practices—they are often legal or regulatory requirements. Board oversight and clear delineation of fiscal responsibility further reduce the risks of errors or unethical conduct. Individuals can replicate these safeguards by automating bill payments, monitoring account balances, and using apps to flag unusual spending patterns.

Leverage Technology for Financial Management

Modern tools have transformed how financial data is managed. Nonprofits benefit from cloud-based accounting software and secure donor management systems, which streamline reporting, simplify audits, and provide real-time insights into their financial status. For individuals, budgeting apps, online investment platforms, and automated savings options improve efficiency and reduce errors. Technology can also free up valuable time, allowing a sharper focus on core missions or personal goals.

Adopting up-to-date technology is critical, as outlined in The New York Times, which highlights how digital tools now empower people to manage and grow their finances with greater transparency and ease than ever before.

Establish Endowments for Nonprofits

Endowments are potent tools for ensuring nonprofit stability over the long haul. By investing a portion of resources, the earnings generated can fund operations and programs indefinitely. Establishing and growing an endowment creates predictable income and sends a message of permanence and stability to donors and stakeholders. For organizations looking to future-proof their mission, pursuing endowment strategies is essential.

An article from Tri-Cities Business News breaks down the practical aspects of creating a sustainable nonprofit endowment.

Prioritize Financial Education

Ongoing financial education is a cornerstone of long-term security. Nonprofits can empower their communities through workshops, seminars, or online resources. Meanwhile, individuals should continuously seek new knowledge about investing, budgeting, and financial planning to adapt as circumstances change. Widely available online courses and local workshops can offer essential updates and refreshers.

The Community Wealth Council is a leading example, helping broaden access to essential financial resources and education for people from all backgrounds.

Adapt to Economic Changes

Staying informed and agile is vital for navigating challenging or changing economic cycles. Nonprofits and individuals should regularly review their financial positions, reassess assumptions, and adjust strategies in light of new information. Ongoing vigilance ensures sustained growth, stability, and an ability to capitalize on opportunities or minimize potential losses. Economic resilience comes from planning and being prepared to pivot when necessary.

Conclusion

Long-term financial security doesn’t happen overnight; it results from innovative, layered strategies. By diversifying income, maintaining strong reserve funds, implementing rigorous controls, embracing technology, building endowments, investing in financial knowledge, and adapting to changes, nonprofits and individuals set themselves up for lasting stability and opportunity. Financial preparedness today forms the foundation for the growth and possibilities of tomorrow.